"The future of banking is not a place you go to, but something you do." – Brett King, futurist and author of Bank 4.0.

What is Virtual Bank?

A virtual bank, also known as branchless banking, operates exclusively through digital channels without any physical branches. This model is gaining traction worldwide, including in Thailand, where the Bank of Thailand (BoT) has introduced guidelines for establishing virtual banks. These banks rely on advanced technology and data analytics to efficiently assess risks and serve their customers. Their primary targets include retail customers, small businesses, and underserved segments that may have limited access to traditional banking services.

Unlike conventional banks, virtual banks focus on digital innovation, offering services such as digital deposits, transfers, and loans. They play a significant role in fostering competition, enhancing efficiency, and improving the overall financial ecosystem. Financial institutions, tech companies, or consortiums meeting specific criteria like good governance, risk management, and digital expertise can operate virtual banks.

Countries like Brazil, the UK, and South Korea have already embraced virtual banks, which provide user-friendly, innovative financial services. In Thailand, the emergence of virtual banks is expected to drive competition, broaden financial access, and offer more personalized financial solutions for diverse customer segments.

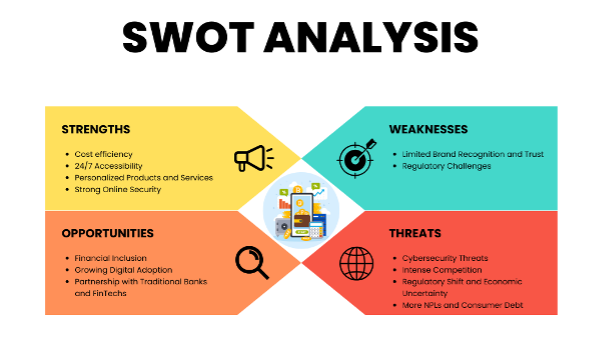

SWOT Analysis

Strengths

Cost Efficiency: As virtual banks do not need for physical, they can significantly reduce service costs leading to lower fees for customers and better interest rates on savings and loans.

24/7 Accessibility: As customers can access services anytime and anywhere via their mobile application or online platform, this improves the accessibility of banking system and benefits the customers with busy schedules and those who live in remote area.

Personalized Products and Services: Without the constraints of traditional banking infrastructure, virtual banks can use AI and data analytics to quickly introduce new products and services based on individual customer behavior and preferences. This creates a more personalized banking experience.

Strong Online Security: Virtual banks prioritize cybersecurity to protect their customers’ data and prevent fraud. They invest heavily in advanced security measures including encryption, authentication, and fraud detection systems.

Weaknesses

Limited Brand Recognition and Trust: Virtual banks are new in the market; they may struggle with brand recognition and royalty compared to traditional banks that have been operating for many years. Furthermore, they may face a significant challenge in building trust among consumers, particularly in older generations who are accustomed to traditional banking and face-to-face interactions.

Regulatory Challenges: Virtual banks may meet unique regulatory difficulties, especially in countries with established banking systems, such as compliance with licensing requirements, data privacy laws, and consumer protection regulations.

Opportunities Financial Inclusion: Virtual banks can help reduce the gap for individuals and businesses that are unbanked or underserved by traditional banks. As customers need less time and documents to open an account, virtual banks can extend financial services to rural areas where they are limited to formal banking.

Growing Digital Adoption: There are more people using digital devices and services; presenting more opportunity for virtual banks to expand their customer base and attract a wider range of customers.

Partnership with Traditional Banks and FinTechs: Virtual banks can partner with traditional financial institutions which already have resources and customer bases to enhance service delivery and expand market reach. While collaborating with fintech startups can help virtual banks with innovative products and services, for example, peer-to-peer lending, cryptocurrency trading, and budgeting tools. These collaborations can keep virtual banks to be competitive and meet the constantly changing needs oof their customers.

Treats

Cybersecurity Threats: As virtual banks are digital in nature, they are more vulnerable to cyberattacks such as data breaches and fraud. They must invest in robust security measures and stay vigilant and proactive to protect their customers’ data, digital infrastructure, and prevent cybercrime.

Intense Competition: The rise of fintech creates a highly competitive environment. Traditional banks also rapidly expand their digital services and offer similar services as virtual banks. These can put pressure on virtual banks to differentiate themselves and provide superior value.

Regulatory Shift and Economic Uncertainty: New compliance requirements and restrictions or changes in economic landscapes can affect virtual banks’ business models, profitability and customer confidence.

More NPLs and Consumer Debt: Despite providing easier access to credit, virtual banks also carry a higher risk of non-performing loans (NPLs) and rising consumer debt if borrowers default on their repayments. To prevent excessive debt burdens among vulnerable populations and ensure overall financial well-being, virtual banks must adopt responsible lending practices.

Global Trends of Virtual Banks

Virtual banking is a rapidly expanding trend driven by technological advancements and the growing adoption of digital financial services. Neobanks, such as N26 in Germany, Monzo and Revolut in the UK, and Chime in the US, have garnered millions of users due to their convenience, low fees, and user-friendly interfaces. These banks offer features like real-time spending analysis, personalized financial advice, and international money transfers at lower costs, particularly appealing to younger generations. In developing regions like India and Kenya, FinTech leaders such as Paytm and M-Pesa have been instrumental in promoting financial inclusion by providing easy banking solutions to millions of previously unbanked individuals. The increasing acceptance of open banking regulations further fosters collaboration between virtual banks and FinTech firms to deliver customized financial solutions to diverse customer needs.

Thailand’s Landscape

Thailand is at the forefront of digital transformation in Southeast Asia, with the rise of virtual banks set to accelerate this trend. With high smartphone penetration and growing internet usage, Thai consumers have become more comfortable with digital financial services, a trend accelerated by the COVID-19 pandemic, making Thailand an ideal market for virtual banks.

Trends Among Thai Citizens

According to the Financial Access Survey 2022 conducted by the Bank of Thailand, while many Thai citizens have access to formal banking services, significant portions of the rural population remain underserved. With fewer traditional banks in these regions, many rely on informal financial services like local lenders and community savings groups. Virtual banks can fill this gap by offering mobile-first banking solutions, making it possible for individuals in remote areas to open accounts, make payments, and apply for loans using their phones.

Impact on Thailand’s Financial Landscape

For Thai consumers, virtual banks offer unparalleled convenience, affordability, and accessibility. With fewer fees, faster service, and more personalized financial products, Virtual banks can empower consumers to save more, access credit easily, and manage their finances effectively. These digital banks also have the potential to transform financial access in underserved areas, promoting financial inclusion and reducing dependency on informal lenders.

However, easier access to loans presents challenges if borrowers struggle with repayments. Virtual banks must prioritize responsible lending to avoid an increase in non-performing loans (NPLs) and rising household debt. Regulators and banks should also emphasize financial literacy to help consumers make informed borrowing decisions.

On a broader scale, traditional banks in Thailand are responding to the rise of virtual banks by accelerating their own digital transformations. This includes developing mobile banking apps, reducing fees, and partnering with FinTech firms to offer innovative financial products. The competition between virtual and traditional banks is beneficial for consumers, offering more financial management options at lower costs. Nonetheless, both types of banks must collaborate to ensure that consumers’ financial well-being is a top priority.

Virtual banks are transforming the financial landscape, offering innovative solutions that address the limitations of traditional banking. In Thailand, they have the potential to boost financial inclusion, enhance customer experiences, and drive economic growth. However, ensuring security, managing risks, and promoting financial literacy are essential for success. As competition grows, the future of banking will depend on how well both virtual and traditional banks can innovate and meet the needs of all customers.

The future of banking isn’t just virtual – it’s limitless.

Photchanan Chewparnich

Digital Investment Promotion Division

Digital Economy Promotion Agency

AI tools were used to check grammar and style to ensure clear and professional communication.

Reference